“I love being British but our railways are shocking. We are so inured to how appalling our railways are.”

Chris Tarrant

The title of this article will generally conjure up thoughts of delays, overcrowding, complicated ticketing and eye watering prices. Our railways are the most expensive cost per mile in Europe and the slowest. Try catching a train over a weekend or on a bank holiday and more often than not the timetable will be in tatters because of engineering works. The morning after a bank

holiday or weekend is normally blighted with engineering works overrunning. Perhaps the most ridiculous thing about our railways is that a number of other country’s nationalised railways

own chunks of the UK’s for profit that is in turn used to make their own railways cheaper.

Before the Pandemic the rail industry received about £4 billion in annual taxpayer subsidies. During COVID the Treasury has had to prop up the railways with nearly £15 billion of taxpayer’s

money. Overall passenger numbers are near 80% of pre-pandemic levels but not on the commuter networks into London, which used to bring in guaranteed season ticket revenues. As

Jacob Rees-Mogg, the Minister for Brexit Opportunities and Government Efficiency (don’t laugh), has found out, it is hard getting people back to their offices on a full-time basis. The

problem is that the financial planning and ticketing costs have been based around commuters being skinned with hugely expensive season tickets.

The government has told the railways that it must reduce costs by 10%. The government owned Network Rail, which manages the infrastructure, is looking at saving £100m a year through

workplace reform. One of the big “work place reforms” will be changing the maintenance regime to a “risk-based” assessment and using more technology, rather than having so many

humans working at weekends. I can just see a drone flying up and down a railway line checking for whatever needs to be checked.

This is where the rail unions come in. Without a concrete proposal having been put forward the largest rail union, the RMT, has already balloted roughly 40,000 members and 16 train

operators for industrial action over pay and cuts. The RMT has to give notice, so any strikes will start in late June, just in time for the summer holidays. Just like inflation, rail strikes remind me

of the nineteen seventies. In fairness rail workers pay has been frozen since 2020 and inflation has risen sharply since then.

The almost impossible dilemma facing Grant Shapps, the Secretary of State for Transport, is how to bring about a 10% reduction in costs without causing a national rail strike. I do not

believe that the railways will ever be able to function without a large annual taxpayer subsidy and it is unlikely that the RMT is going to accept new working practices without a thumping pay

rise for its members.

So, what do we do this Summer? Fly off to sunnier climes and undergo the agony of being mucked around for hours or even days in overcrowded airports. You could drive to the seaside

in the UK but that will probably entail hours of sitting on one of our motorways and with the cost of petrol burning a hole in our pockets we may not be able to even afford fish and chips.

The likely hood of rail strikes this summer means that even city breaks will carry a high degree of travelling uncertainty. It is going to be a case of it being better to arrive than to travel. Happy

holidays!

We expect the global economic recovery will continue to disappoint, with growth well below consensus expectations across the major economies. Despite soft economic activity, most major

central banks will continue to tighten monetary policy aggressively to combat above-target inflation. Commodity prices will remain high amid supply disruption, benefitting economies which export raw materials at the expense of importers. Europe will flirt with a recession as the economic fallout from the war in Ukraine bites, while China's economy struggles with lockdowns, a property slump and fading export demand.

While the worst of the bond market sell-off is probably behind us, we expect core government bond yields to rise further as the global tightening cycle continues. But with discount rates rising and

economic growth disappointing, the outlook for risky assets remains fraught. While equity market valuations have fallen, they still look elevated relative to the past, at least in the US. With analysts’ expectations for firms’ earnings still looking quite rosy, there is ample room for disappointment as the global economy slows. Rising bond yields means that the rotation from “growth” to “value” stocks will continue as the rate-sensitive tech sector falters and more defensive sectors hold up best.

The combination of aggressive tightening from the Fed and worsening risk appetite has driven the dollar to its strongest level, in aggregate, since the early 2000s. We expect it to extend those gains as major central banks struggle to match the Fed’s hawkishness and economic growth slows more sharply in Europe and Asia than in the US. The hawkish tone of the latest ECB and Fed speakers suggests that, despite the recent drop in equity markets and widening of credit spreads, policymakers are determined to press ahead with aggressive monetary policy tightening. In

particular, the ECB, having been slow out of the gate, appears to be playing catch up. We think those hoping for a “Fed put” to stave off further equity market weakness will be disappointed. Chair

Powell’s recent comments suggested that the FOMC is not overly worried by this year’s fall in US equities. Falling prices of financial assets is a key channel for conditions to tighten. Likewise, it

appears that the surge in inflation has shifted up the ECB’s and Bank of England’s pain thresholds with respect to periphery spreads, allowing them to tighten rates.

Sanctions and extreme economic uncertainty have already crippled Russia’s economy and financial markets. Russian assets generally will probably remain un-investable for Western investors for some time. But, while financial conditions have tightened elsewhere as well, the global financial system has so far proven resilient. We think that will remain the case, and that in the event of a more material deterioration of market functioning central banks would step in quickly to restore stability.

We also don’t anticipate significant spill-overs to most major EMs – many of the economies where balance sheets look most vulnerable are commodity exporters (e.g. Brazil and South Africa), which will benefit from the surge in commodity prices, improving their ability to weather this storm. Turkey faces the greatest risks: its financial situation has been precarious for some time, it has significant trade links to Russia, and imports most of its energy needs.

The combination of hawkish central banks, rising bond yields, and faltering growth has proven challenging for most risky assets, which have fallen sharply this year. The “stagflation-lite”

environment now taking hold means further pain is in store: equities will not turn the corner decisively until central banks ease off on policy tightening and fears of a major global downturn fade.

We think the equity markets may still be vulnerable as the global economy slows and more companies struggle to meet optimistic earnings expectations. The latest leg down had all the

hallmarks of a growth scare: bonds rallied as investors unwound bets for rate hikes, while safe-haven currencies strengthened. Previous weakness can be pinned on rising “safe” asset yields as investors absorbed the Fed’s hawkish pivot, which piled downward pressure on equity valuations despite

continued earnings growth.

So we navigate the summer with a more modest attitude to risk in our portfolios – shortening the duration of bond holdings and keeping exposure to commodities and the value-based, previously

underperforming UK equity market. Valuations are more modest today, but we do not see the catalysts for recovery in markets at this stage.

|

UK Equities: The UK equity market has returned its gains of the early months of this year, despite its relatively modest valuation and the resilience of leading international companies after a period of post Brexit doldrums. War on the eastern edge of Europe, sponsoring inflation, supply chain disruptions and heightened security risks, have led equity markets into a more volatile phase. The UK market is holding up better than many developed market peers, although this reflects a number of years of relative underperformance. Despite a strong earnings and cashflow recovery from the lows of the COVID crisis, rising inflation pressure implies more tightening of monetary policy this year. Nonetheless, the relative cheapness of UK equities leads us to expect the UK to play catch up to other developed markets. |

|

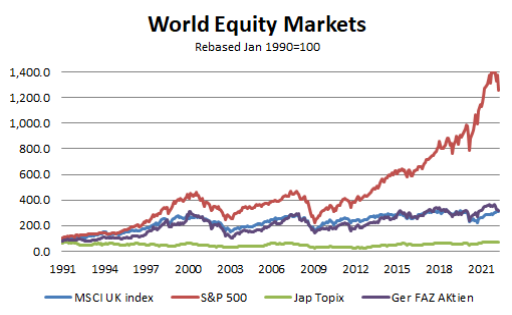

World Equity Markets: International equity markets in general carry higher valuations than the UK. At a time when ongoing economic recovery is weakening globally among signs of higher inflation across the world, many leading equity markets have suffered falls in the early months of this year. Central bank policy accommodation in Europe and the US is being moderated in light of inflation risks. The Ukraine war adds to commodity prices and supply chain disruptions. In the US, there is a risk that robust earnings growth may weaken, that labour markets are tight and consumers may start to rein back spending in light of inflation concerns. Japanese markets may encounter inflation for the first time in a generation. EM stocks will have to overcome logistical disruptions and price pressures, which combine with reduced investor risk appetite to overshadow equity markets through the coming months. |

|

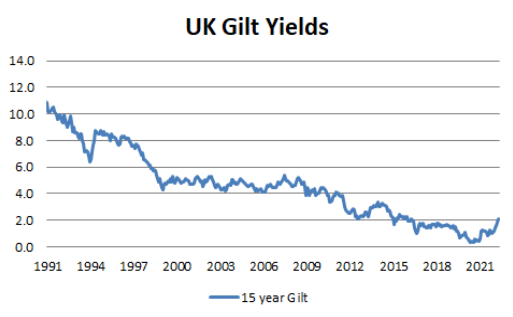

UK Gilt Yields: Gilt yields continue to rise at both the short and long end of the curve – the 10-year gilt has risen by 65 basis points over the last three months and currently yields 1.86% to redemption. Despite investors rotating to lower risk government securities in light of geopolitical risks, inflation concerns reflect shortages of materials and wage pressures, given labour shortages in sectors, such as retail and hospitality. Real gilt yields are very negative, given high headline and core inflation. Markets are concerned that the Bank of England is not on top of inflation management and will be looking closely at the risks of policy error, given the need to balance economic recovery and housing affordability against significant inflation risk. |

|

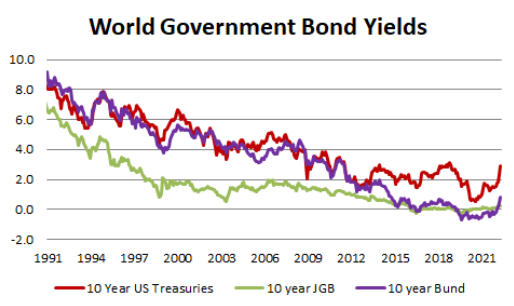

World Government Bond Yields: We think the rises in global government bond yields have a little further to run. Government bond yields have typically peaked only shortly before the ends of central bank tightening cycles and we expect most major central banks to continue hiking rates over the next 12 months or so. The increase in government bond yields, as well as the threat of slowing global economic growth, will keep corporate bonds, under pressure. We also expect the worsening risk environment as well as particularly aggressive tightening by the Fed to result in a further strengthening of the US dollar. We suspect bond markets will only start to turn a corner around the middle of next year as tightening cycles draw to a close. |

|

Uk Short term Interest Rates: Our forecast that the Bank of England will raise interest rates from 1.00% now to 3.00% next year is higher than the peak of 2.50% priced into the market and the peak of 2.00% expected by many analysts. We think the economy will just about avoid a recession. But more importantly, we expect the unemployment rate to remain lower for longer, wage growth to be higher and the recent increases in price and wage expectations to prove sticky. These combine to keep inflation pressures elevated for a while. |

|

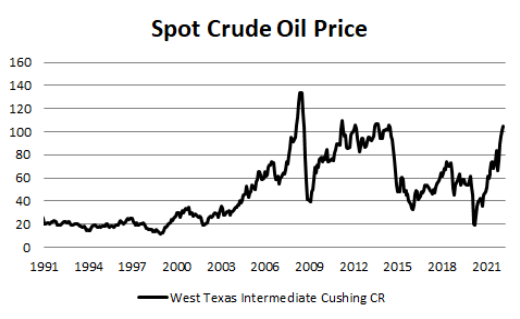

Spot Crude Oil Price: We think energy prices will stay historically high this year, regardless of the outcome of the war in Ukraine, as we expect the West to persist with plans to reduce its dependence on Russian energy. This process will disrupt existing supply chains and prove costly. That said, we expect the price of oil to start to ease back as we move into 2023 and supply responds to higher prices and demand growth slows. But there are major risks to the upside for energy prices given the uncertainty surrounding the war in Ukraine. The last time prices were this high, US shale drillers were pumping flat out and OPEC countries and allies were locked in a battle for market share. |

|

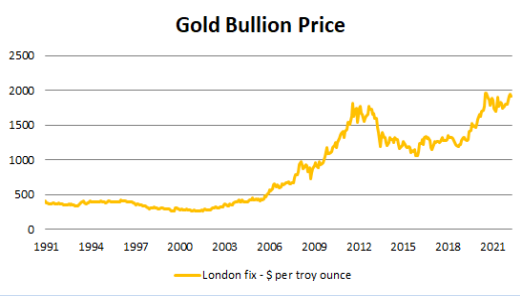

Gold Bullion Price: As a real asset, gold is a classic safe haven in times of geopolitical uncertainty and inflation risk. Physical demand for gold has remained strong and investors are looking to this asset for portfolio insurance at a time when risk assets are suffering. ETF buying has picked up. Central banks’ gold purchases have remained strong on their view that gold is a valid asset for reserve management of inflation risk. The price of gold will be vulnerable if inflation levels ease back and the historic inverse relationship with US real yields is restored. But we do not see this happening for a while. |

Note that where an MSCI Index has been used for illustration. This has been sourced with permission from MSCI Inc.

| ISA Allowance 2021/2022 | Stocks & Shares ISA

Cash ISA Junior ISA |

£20,000

£20,000 £9,000 |

| Pension Allowance 2021/2022 | The limit is the greater of £3,600 and 100% of salary, subject to the annual allowance of £40,000 (unless money has been accessed through flexi drawdown in which case the annual allowance is limited to £4,000). |

| Income Tax | Personal Allowance 2021/2022

Basic Rate @ 20% Higher Rate @ 40% Additional Rate @ 45%

Married couple’s allowance: Older spouse born before 6 April 1935 |

Up to £12,570 £12,571 to £50,270 £50,271 to £150,000 Over £150,000

Minimum £3,530 Maximum £9,125 Up to 10% of the appropriate Min/Max |

| Capital Gains Tax | Annual Exemption – Individuals

Basic Rate tax band (residential property) Basic Rate tax band (other assets) Higher Rate tax band (residential property) Higher Rate tax band (other assets) Business Asset Disposal Relief Business Asset Disposal Relief limit of gains |

£12,300

18% 10% 28% 20% 10% £1,000,000 |

| Inheritance Tax | Threshold up to £325,000

Over £325,000 |

Nil

40% |

| Corporation Tax | Full Rate

Small Companies Rate (SCR) |

19%

19% |

GHC Capital Markets Limited · Investment Managers & Stockbrokers · 22-30 Horsefair Street, Leicester LE1 5BD

Telephone 0116 204 5500 · www.ghcl.co.uk

The information given is of the opinion of GHC Capital Markets Limited, the opinions constitute our judgment which are subject to change. This document is for the information of clients and prospective clients and is not intended as an offer or solicitation to buy or sell securities. The information given is believed to be correct but cannot be guaranteed and opinions constitute our judgment, which is subject to change. Certain investments carry a higher degree of risk than others, are less marketable and therefore may not be suitable for all clients who should always consult their investment adviser before dealing. The value of stocks, shares and units and the income from them may fall as well as rise and this also applies to interest rates and the Sterling value of overseas investments. Past performance is not necessarily a guide to future returns and investors may not get back the amount they invested. Any anticipated tax benefits depend upon an individual’s

circumstances and are subject to changes in legislation and regulation, which cannot be foreseen. Directors, employees and other clients of GHC Capital Markets Limited may have an interest in securities mentioned by the firm but all officers operate a policy of independence which requires them to disregard any such interest when making recommendations. Note that telephone calls may be recorded.

COPYRIGHT: © GHC Capital Markets Limited, 2019. All rights reserved. No part of this publication may be reproduced, transmitted,

transcribed, stored in a retrieval system, or translated into any language in any form by any means without the written permission of GHC

Capital Markets Limited.